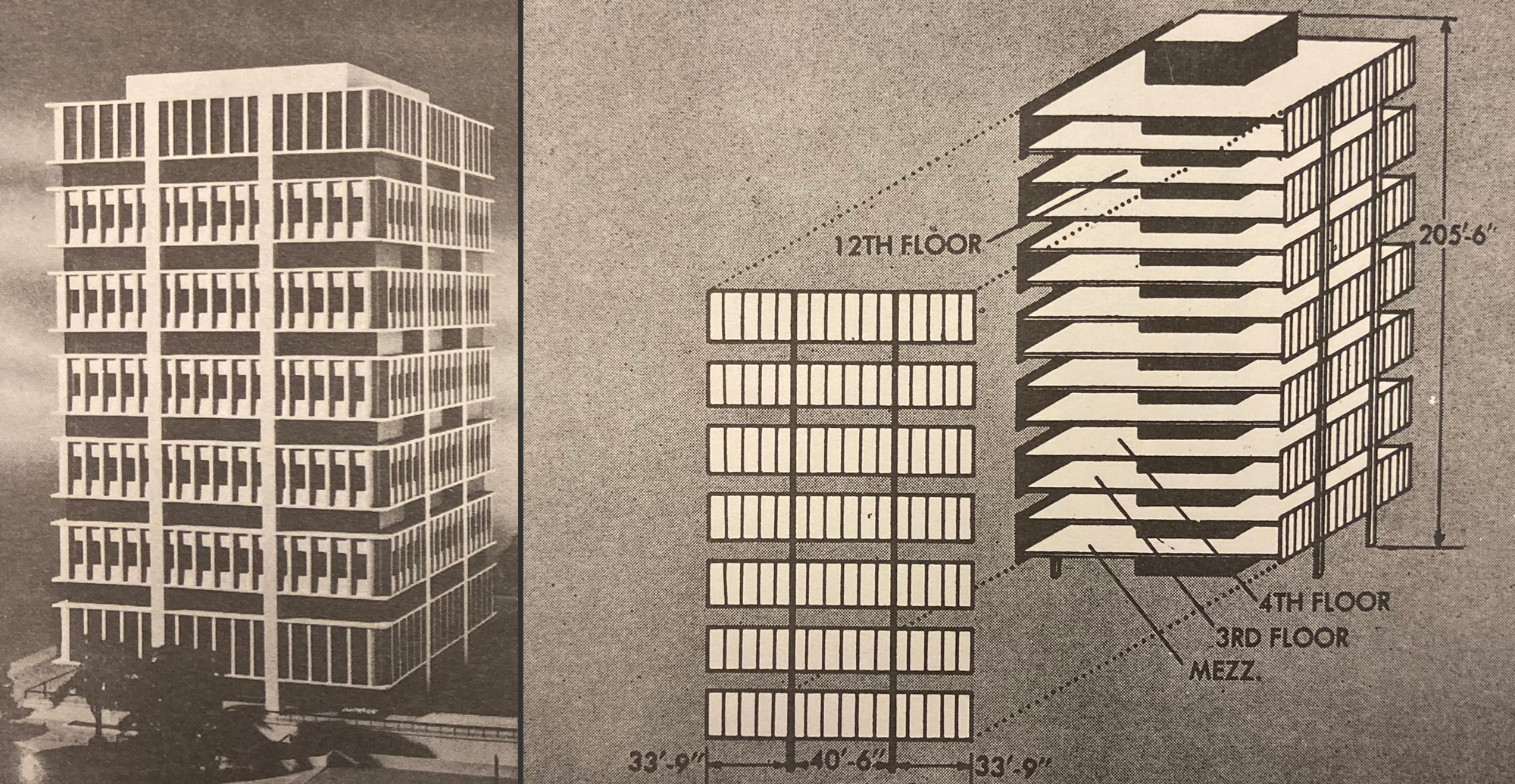

In April, 1966, North Carolina Mutual Life Insurance Company hosted a five-day ceremony to inaugurate the opening of the first Black skyscraper in the United States. 1 At twelve stories, the NC Mutual building rose impressively above the low-rise skyline of the city of Durham, marking more than a half-century of growth for the nation’s largest company owned by African Americans.

Revolutionary thought proposes fundamental ruptures with the past. Actuarial thought adumbrates the future according to the patterns of the past.

Like all towers, the NC Mutual building projected visions of the future, not only as a capital investment, but also through the social and technical imaginaries it suggested. These futures were bound up, on one hand, with the actuarial methods of risk assessment practiced by insurance companies and, on the other hand, with antiracist struggles that had by the mid-1960s acquired revolutionary momentum. The NC Mutual tower, and the enterprise it represented, were therefore caught between two epistemologies — actuarial and revolutionary thought — each envisioning the future in terms of a particular relation to the past. Whereas revolutionary thought proposes fundamental ruptures with the past, actuarial thought adumbrates the future according to the patterns of the past. Insurance companies and their mortgage-lending subsidiaries determine which types of people and places constitute promising objects of investment by examining past and present trends in incomes, life expectancies, and housing markets. In the U.S., these trends have of course been shaped by centuries of racial discrimination and violence.

One of the nation’s first actuaries, Frederick Hoffman, had published a treatise in 1896 arguing that African Americans should be insured at higher premiums because of their higher death rates, a datum Hoffman ascribed to innate racial degeneracy. 2 Yet actuarial practice does not require recourse to biological racism in order to naturalize discrimination. It needs only to be actuarial: to sort people by race, gender, occupation, geography, or income; to interpret these groups’ past and present disadvantages as predictive of future ones; and, on those grounds, to deny benefits that might otherwise help such groups to overcome historical disadvantages. 3

In attempting to combat structural racism through actuarial practice, Black insurance companies were thus entangled in a double bind. As early as 1923, in an in-house publication titled Statistical Bulletin, NC Mutual staff described the predicament of African American insurance:

The real problem which faces a Negro Life Insurance Company is the finding of sufficient lives to insure among persons who have both the economic ability to pay and the health to insure …. By the time a Negro becomes able to maintain a few thousand dollars’ worth of insurance, his health has been so undermined through long hours of toil and years of self-denial that he is not a fit physical risk. 4

Again and again in their promotional materials and correspondence, African American insurance companies claimed to correct racial inequities in health and poverty. Yet they could only do so by offering policies to families with better-than-average prospects, lest they put their own businesses at risk.

African American insurance companies often claimed to correct racial inequities. Yet they could only do so by offering policies to families with better-than-average prospects.

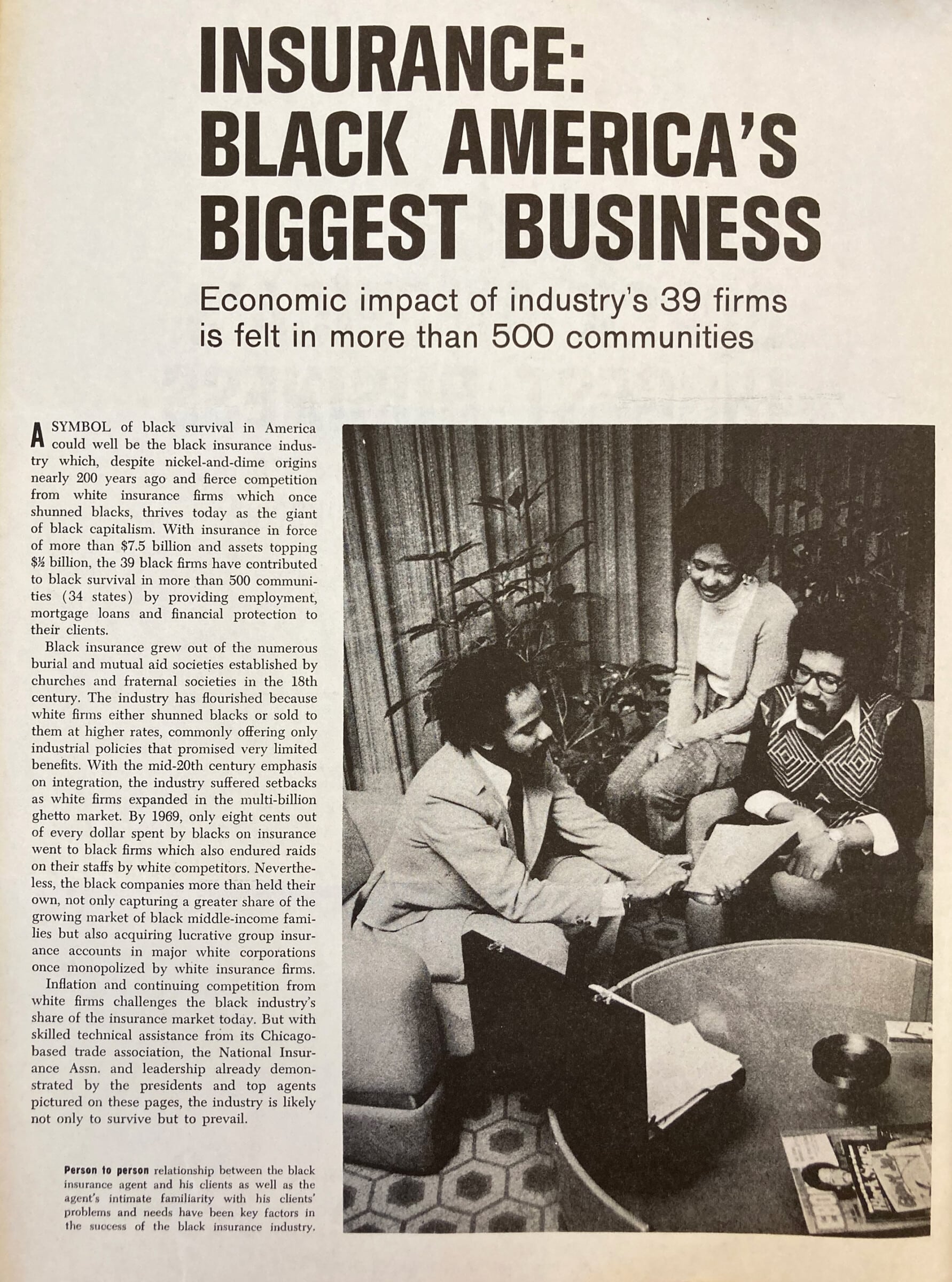

From the 1920s through the 1970s, the Black-owned insurance industry controlled more wealth than any other form of African American business, and played a crucial role in supporting urban and suburban development for African American communities. By 1933, 40 companies were headquartered in 32 cities (mostly in the southeast), serving a primarily working-class clientele. At the sector’s peak in the late 1950s, the number of firms had almost doubled, following the rise of working-class wages in the postwar years. Executives at these firms maintained a delicate balancing act within evolving contexts of racial capitalism, hewing to actuarial forms of thought that tended to deepen class divides, even as they agitated in various ways for civil rights. Such complex and at times paradoxical efforts speak to longstanding debates about whether it is possible to extirpate the racial component of racial capitalism, while leaving the system otherwise intact.

Civil rights issues often dovetailed with insurance firms’ self-interests, since they needed reasonably healthy and financially stable people and places to invest in. That said, activism within the African American insurance sector generally exceeded what might be expected from pure financial calculation. Many company directors dedicated immense time and financial resources to supporting political causes, often without much likelihood of success. Executives from NC Mutual joined their counterparts at firms like Atlanta Life Insurance, Supreme Liberty Life Insurance (in Chicago), Golden State Mutual Life Insurance (in Los Angeles), and Universal Life Insurance (in Memphis) in maintaining close ties with the National Association for the Advancement of Colored People, the Congress of Racial Equality, and the National Urban League.

Some executives assumed leadership positions at these organizations; some played vital roles in other ways. Supreme Life’s president Earl Dickerson defended housing integration in Supreme Court hearings, while Atlanta Life’s president Jesse Hill led voter registration drives and personally donated money to bail Martin Luther King, Jr. out of jail. 5 The companies also provided economic support to hundreds of local and regional institutions, including historically Black colleges and universities, churches, and the YMCA; their leaders served in dozens of civic and governmental bodies, including the Los Angeles City Housing Authority, the Chicago City Council, the Atlanta Chamber of Commerce, and the Metropolitan Atlanta Rapid Transit Authority.6

Interpolated within a dense civic network, Black insurance companies filled a vacuum left by governmental dereliction, functioning as a kind of shadow state.

Recent histories of the White-owned insurance industry have critiqued its biopolitical tendencies in the 20th century, as it assumed tasks of wealth redistribution and the provision of healthcare and housing that might otherwise have been performed by the state, in a manner more accountable to democratic processes. 7 To some degree, the same could be said of the African American insurance industry: that it arrogated issues of public concern to the purview of private corporations. It is critical to recall, however, that political power among African Americans was so suppressed in these decades that, in many cases, political causes had to be pursued through extra-political means. Interpolated within a dense civic network, Black insurance companies filled a vacuum left by governmental dereliction, functioning as a kind of shadow state.

In 1907, W.E.B. Du Bois had lauded the role of such businesses, describing their evolution from mutual-aid and fraternal societies that pooled resources to provide for members’ unexpected household expenses, such as funeral costs. 8 In the decades between the wars, the influx of African Americans into the industrial workforce supported the expansion of what was called “industrial insurance,” offering compensation for household wage loss in the case of a breadwinner’s injury or death. Because White-owned companies often discriminated against African American applicants, charging higher premiums or refusing coverage outright, Black-owned firms expanded in tandem with the urbanizing population.

Firms operated in a variety of contexts, from the Jim Crow south to the northern and western cities that were destinations in the Great Migration.

An analogous situation existed in the realm of housing and commercial real estate, as African Americans struggled against restrictive racial covenants, redlining, discriminatory rents, and lack of access to mortgage lending. In response, Black insurance firms invested in urban and architectural development, financing office buildings and sometimes sponsoring their own housing developments, often using African American architects or contractors. Many had their own mortgage-lending departments; some insurance executives also co-owned or held major stakes in separate savings-and-loan businesses that offered mortgages. Across such operations, company directors had to choose when, and to what extent, to follow or to flout mainstream — that is, White — prescriptions of risk, e.g. in regard to housing-market trends that disadvantaged African American neighborhoods. As African Americans were often excluded from formal channels for real estate development, city planning, and architectural production, Black insurance companies assumed many of the responsibilities associated with urban development. Just as these companies functioned as a shadow state in regard to wealth redistribution, they acted as “de facto urban planners.” 9

I’ve been discussing Black-owned insurance companies as a single group — and, indeed, their leaders maintained collegial contact through the National Insurance Association, an alliance of African American firms. However, these firms were guided by distinct and shifting directorial visions, as they operated in a variety of contexts, from the Jim Crow South to the northern and western cities that were destinations in the Great Migration. Contextual differences were not reducible to differences between south and north. Cities like Atlanta and Chicago supported robust African American civic and political networks, formed in response to racial violence, segregation, and housing shortages. Durham, on the other hand, had been praised by Du Bois in 1906 for its peaceful race relations and prosperity; perhaps because of this relative calm, it was not a major site for civil rights politics until the sit-in movements of the 1960s. In their role as shadow states, the insurance companies were differently situated within their respective civic networks, and they responded differently to the politics of civil rights.

Certainly debates about race and capitalism loomed large in 1966, the year that NC Mutual opened its Durham tower. Fissures were deepening between radical and conservative contingents in the civil rights movement; that year witnessed both the birth of the Black Panthers and a growing interest in Black capitalism. The latter term comprehended diverse attitudes and strategies, including forms of cooperative enterprise and “buying Black.” But when promoted by conservative African Americans, not to mention White politicians like Richard Nixon, “Black capitalism” usually suggested the extension of market-based opportunities, without the need for structural transformation. 10

The unveiling of NC Mutual’s tower seemed to trumpet the ascent of this type of Black capitalism. The keynote address, by U.S. Vice President Hubert Humphrey, pointed to NC Mutual as a harbinger of racial success, while other speakers praised the corporate tower as a concrete refutation of Black Marxist critiques. 11 Yet the topic was up for debate even among speakers at the dedication. Andrew F. Brimmer, the first African American to serve on the U.S. Federal Reserve Board, was a devout Keynesian, and hardly a leftist. Still, he warned his audience against Black capitalism as a path toward economic betterment, given the dwindling wages and employment opportunities faced by the generation then coming of age. 12

From a different perspective, the prominent Durham journalist Louis Austin later noted that steep rents made office space in NC Mutual’s tower inaccessible to Black businesses; the local community complained that the lavish opening ceremony excluded ordinary African Americans. 13 In response to such criticisms, the president of NC Mutual, Asa T. Spaulding, tended to repeat the mantra of his corporate predecessor (and distant cousin), Charles Clinton Spaulding: the company was “owned by its policyholders.” 14 As directors of a mutual or profit-sharing corporation, Spaulding insisted, he and his colleagues were not in the business of enriching themselves. Rather, they were mere “employees” of a company dedicated to lifting working people into middle-class stability.

The Actuarial Double Bind

Though guided in important respects by civic responsibility and public opinion, African American insurance companies were also, by their nature, beholden to market trends, market predictions, and the probabilistic science of actuarial calculation. These tools were used to sift out supposedly good risks from bad ones in regard to life expectancy, mortgage lending, and urban development. Du Bois had observed early in the century that Black insurance firms were kept afloat by a high rate of policy lapses: clients unable to maintain weekly payments had to forfeit policies before they could make claims. It was also true, however, that depending on how long a policy had been held, its lapse could be detrimental to the firm, given the expense of soliciting and processing new accounts. 15 Du Bois remarked that companies were therefore handicapped by the “unscientific basis” of their operations — but that, fortunately, some were beginning to adopt “graduated payments on a scientific age classification.” 16 That is, they had taken an actuarial turn.

By the late 1930s, U.S. housing policies were increasingly a channel through which racialized risks — and indeed, raciality itself — were produced.

Asa T. Spaulding was hired as Chief Actuary at NC Mutual in 1932, having become the first African American to earn a master’s degree in mathematics and actuarial science. (Two decades later, Jesse Hill of Atlanta Life would follow suit.) Spaulding began his job by sifting through company records, correlating lapses and payouts to demographic data. 17 Appalled by the discrepancies between policyholders’ projected and actual mortality rates, he established a new committee to stringently review applicants’ health and financial prospects, including stricter enforcement of medical examinations. 18 He urged agents to chat with applicants’ friends and neighbors, to ferret out details concerning “occupation, environment, personal history and habits and reputation — the moral hazard should never be overlooked.” Carelessness on the part of the agent would, Spaulding warned, “result in a warped and imperfect reconstruction of the individual as an insurable risk.” 19 As the actuary’s job was to prognosticate mortality, he was, by Spaulding’s account, “regarded with a certain sense of awe.” 20

Actuarial praxis determined not only which lives to insure at what rates, but what kinds of urban properties to invest in. By the late 1930s, U.S. housing policies were increasingly a channel through which racialized risks — and indeed, raciality itself — were produced. A notorious example was the Federal Housing Administration’s approach to housing development and mortgage lending, which incentivized militant forms of segregation. Thus African American lending institutions had to contend with racial covenants, redlining, slum clearance, and — in the wake of White flight and industrial flight in the postwar decades — spiraling urban disinvestment.

The social and economic capital wielded by the largest companies was vital in combatting the displacement, housing shortages, and ghettoization that resulted. But firms were also understandably wary of financial risks in the urban housing market. Navigating the actuarial double bind led to a range of strategies; some executives tried to combat segregation and redlining, while others adhered to trends toward single-family suburban homeownership. In other words, these latter firms accommodated market demands — yet it is worth noting that such histories reveal the conceptual inadequacy of the category “accommodationist.” In contexts of violent racial oppression, what did it mean to accommodate racial and economic injustice? What other options existed?

Toeing the Redline? Racial Risk and the Housing Market

In 1937, the Chicago-based Supreme Liberty Life Insurance Company issued a mortgage to a Black real estate broker, Carl Augustus Hansberry, for a home in the Woodlawn neighborhood, in defiance of the Woodlawn Property Owners’ restrictive covenants. Hansberry’s daughter Lorraine — only seven years old at the time — would later draw on the family’s experiences of fighting segregation in her famous play, A Raisin in the Sun. 21 Shortly after Hansberry’s real estate purchase, Supreme Liberty’s president, Harry Pace, bought a home nearby, giving the company a major stake in the ensuing lawsuit, Hansberry v. Lee. 22 In this landmark 1940 case, Supreme Liberty’s general counsel (and later president) Earl B. Dickerson successfully argued against the applicability of restrictive covenants to Hansberry’s and Pace’s properties. Dickerson went on to lead Supreme Life in financing mortgages for more Black Chicagoans, compelling desegregation in the city’s Hyde Park and Kenwood neighborhoods. 23

It would be another eight years before Dickerson helped to push the Supreme Court to declare all restrictive covenants legally unenforceable. But many were emboldened by the Hansberry verdict. In Los Angeles in 1938, the treasurer (and later president) of Golden State Mutual, Norman O. Houston, had purchased a house in the upscale neighborhood of Sugar Hill, prompting a lawsuit on the part of the West Adams Heights Improvement Association (or WAHIA). 24 At the same time, other wealthy Black, Latino, and Asian professionals, along with several African American movie stars — Louise Beavers, Hattie McDaniel, Butterfly McQueen, and Ethel Waters — began purchasing homes in the neighborhood. 25

In 1943, African American residents formed the West Adams Heights Protective Association (or WAHPA) to fight WAHIA’s attempt to enforce their restrictive covenants, electing Houston president and Beavers vice president. For their defense, the WAHPA hired the renowned African American civil rights litigator Loren Miller, who argued that restrictive covenants violated the 14th Amendment of the U.S. Constitution. 26 Consequently, in 1945, the Los Angeles Superior Court declared such covenants to be unenforceable in California, setting a precedent for the Supreme Court’s 1948 verdict. 27

In the landmark 1940 case Hansberry v. Lee, Supreme Liberty Life Insurance of Chicago successfully argued against restrictive covenants.

In the southeast, efforts at desegregation and African American expansion proved even more challenging. Nonetheless, directors of Atlanta Life Insurance Company worked with the Urban League and with fellow African American business owners to buy up large tracts for housing expansion. 28 Meanwhile, in Chicago and Los Angeles as well as in Atlanta, desegregation efforts were united not only in contesting ghettoization, but in refusing FHA-driven actuarial frameworks that condemned older, denser parts of cities as poor investment risks. 29 The FHA had created a self-fulfilling prophesy: redlined neighborhoods suffered the deleterious effects of disinvestment. By defying prescriptions that discouraged investment in multifamily housing, rental units, and older central-city areas, companies like Atlanta Life and Supreme Liberty underscored that the FHA’s actuarial powers consisted less in divining risk than in creating and codifying it.

Companies that did tend to follow FHA prescriptions of risk — including NC Mutual and Memphis-based Universal Life Insurance Company — were in effect withdrawing support from crucial social infrastructures in urban cores. From the late 1930s through the ’40s, NC Mutual reports had noted the vast expansion of financial opportunities in suburban housing, recommending the rapid sale of their urban investments and the acquisition of suburban mortgages, developments, and land. 30 In the following decades, the company’s mortgage board rejected virtually all requests to finance the rehabilitation of housing stock in older city centers, especially for multifamily dwellings. At the same time, from 1952 to 1953 alone, NC Mutual’s FHA-backed mortgages for suburban or peri-urban single-family homes increased 75 percent, from two million to three-and-a-half million dollars. 31

Directors of Atlanta Life Insurance Company worked with the Urban League and with fellow African American business owners to buy up tracts for housing expansion.

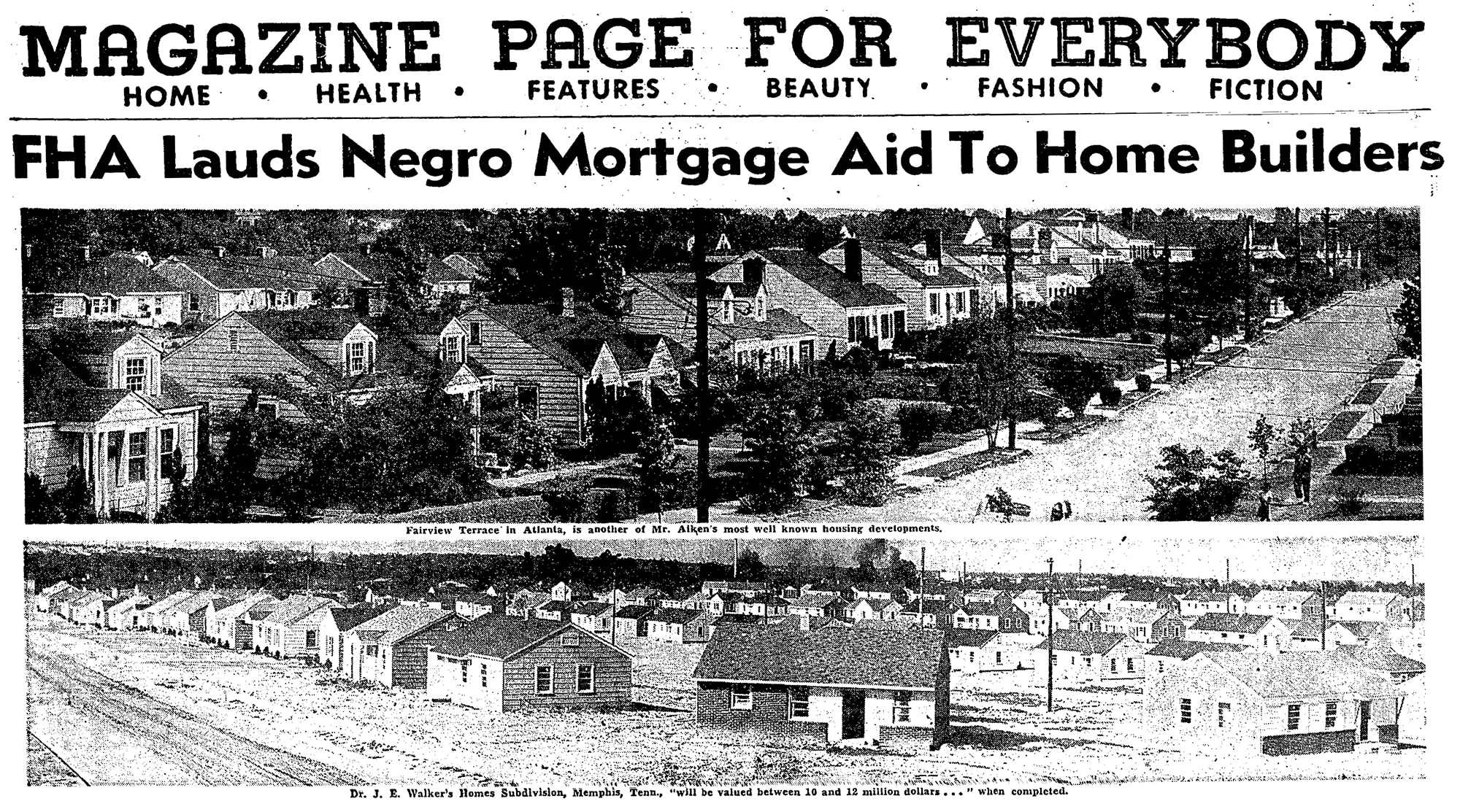

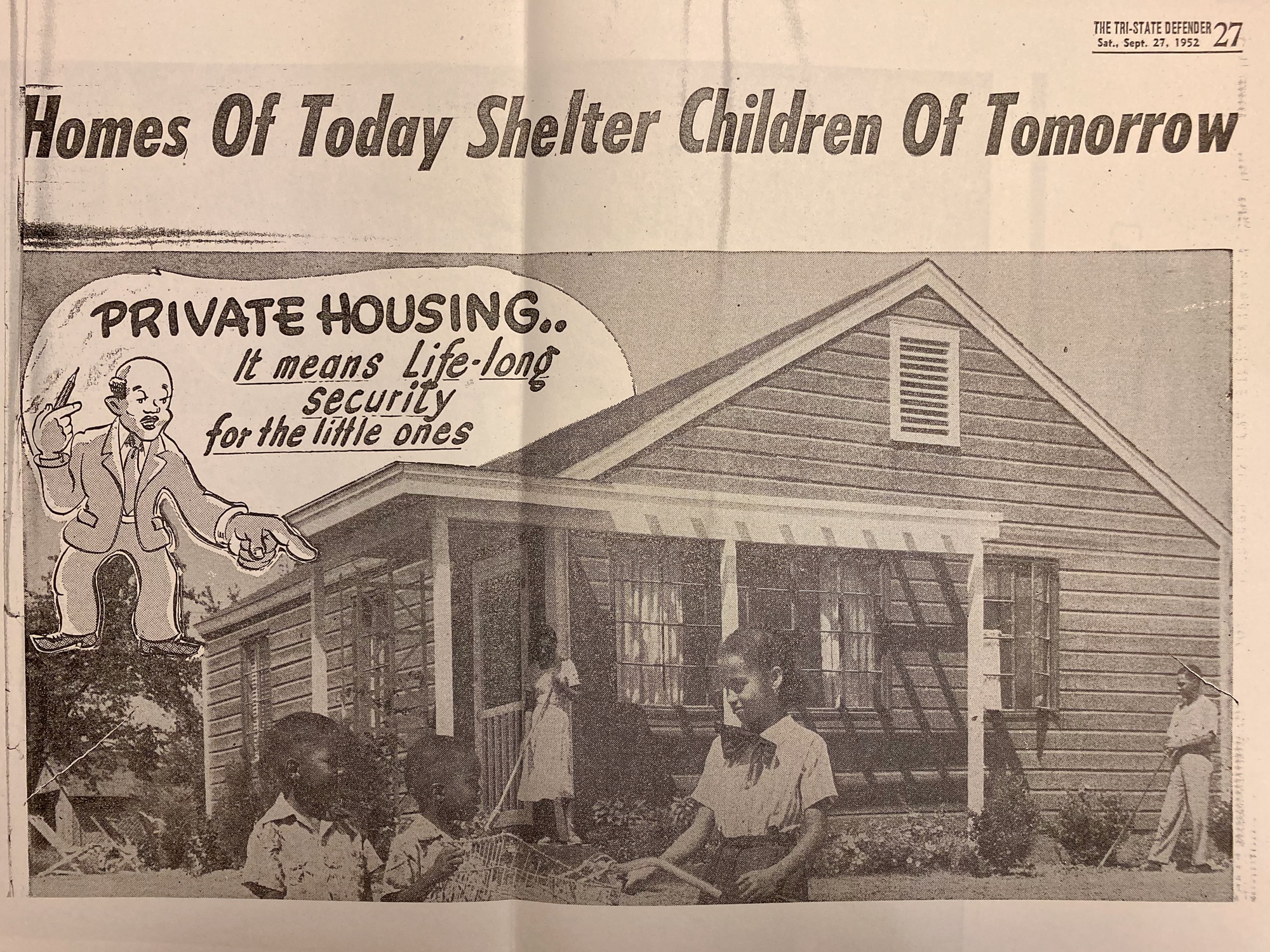

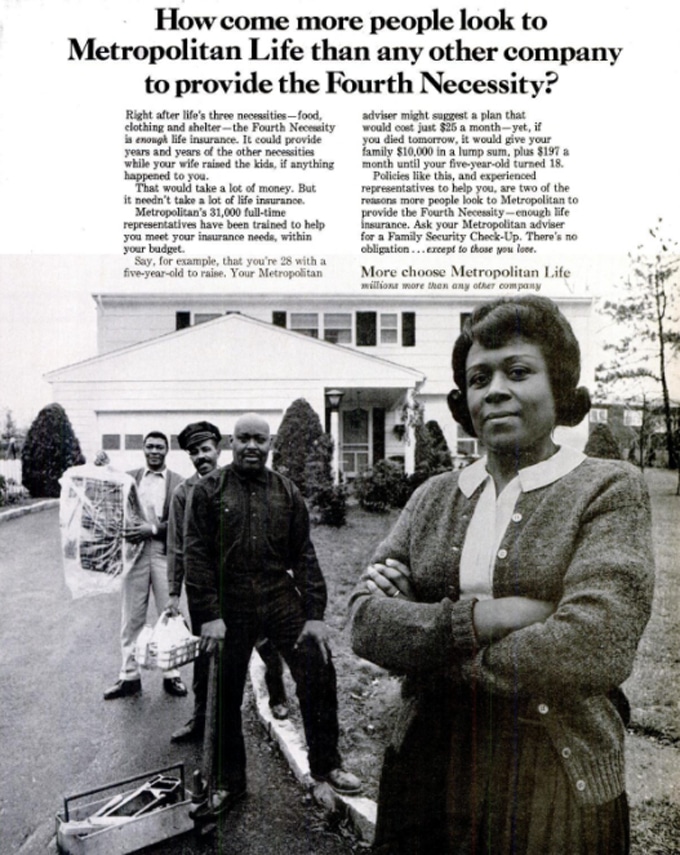

In these years, Black insurance companies were doing more than underwriting mortgages. African American executives knew that, in New York City, the White-owned insurance giant Metropolitan Life had begun constructing segregated housing developments. 32 Apart from serving as investments, these private complexes, nestled in expansive park-like settings, allowed Met Life to provide current and prospective policyholders with healthy, low-rent homes, turning them into better actuarial risks. 33 (In Ebony, Met Life advertised the “Fourth Necessity” — life insurance — directly to Black women heads of households.) Dr. J. E. Walker, founding president of Universal Life, took notice, and commissioned the first of three housing subdivisions for African Americans that he would develop outside Memphis — Riverview Homes, the Walker Homes, and Elliston Heights. Ultimately, with FHA-backed financing, Walker oversaw the construction of 2,010 single-family houses. (In Memphis, a local newspaper ran a composite photo-and-cartoon illustration showing a middle-class Black family enjoying their tidy front yard, while a cartoon likeness of J.E. Walker floats above them, promising “PRIVATE HOUSING: It means life-long security for the little ones.”) Mortgages were underwritten by Walker’s own bank, the Tri-State Bank of Memphis, and by NC Mutual, while Universal Life provided homeowners’ insurance. 34

Walker built in areas that would prompt the least resistance from White Memphians, purchasing tracts on the city’s outskirts, abutting infrastructural buffers that separated the new developments from existing White neighborhoods. 35 In this way, Universal Life provided an opening for “Black flight” — of working-class persons and dollars — from older neighborhoods. Walker’s projects risked justifying suburbanization. This ignored not only the obstacles that segregation and mortgage-lending practices posed to Black suburbanization, but also more radical alternatives, such as racial integration or the infusion of tax dollars into existing Black neighborhoods. That said, by purchasing scattered tracts several miles past the fringes of existing African American districts, Walker sandwiched a huge section of Memphis between those extant neighborhoods and his new developments, effectively bounding the city’s southwestern quadrant as a domain for African American expansion. 36

The actuarial double bind compelled Black developers to choose between the risks of investing in redlined neighborhoods, and complicity with the logics of redlining and suburbanization. Walker’s projects helped redress the city’s shortage of African American housing, but also furnished convenient examples to White politicians and policymakers who wished to show the efficacy of relying on private markets to solve the housing crisis. 37 Publicity for Walker’s developments mimicked Cold War propaganda that cast public housing as “communist.” This “suburban turn” also came at the cost of measures that might have helped compel integration. As the founding Secretary of Housing and Urban Development, Robert C. Weaver, observed in 1956, rent-controlled housing tended to promote integration, since it incentivized White residents to remain in their units after other groups moved in. Private housing did the opposite, as homeowners dreaded the possibility of market depreciation. That is, White homeowners — regardless of personal racial prejudices — acted on actuarial fears of racial risk. 38

Reverse-Redlining: Corporate Architecture as Conspicuous Investment

Some Black insurance companies took a different tack, standing against market trends that favored urban disinvestment. In the early 1950s, for instance, Atlanta Life withdrew from the FHA-backed mortgage market while helping to finance rental housing projects in older center-city neighborhoods. One such complex, Magnolia Terrace, was a set of low-rise apartment blocks surrounded by green space, in which 44 new three-bedroom units were leased at $42.50 per month (about $560 in 2024 terms). 39 The project was located just north of Atlanta University, an historically Black institution encircled by a narrow ring of middle- and upper-class Black-owned homes — among them the estate of Atlanta Life’s founding director, Alonzo Herndon, who had been born into slavery, built up a real-estate empire, and was then Atlanta’s wealthiest African American. While this concentration of affluence did not prevent the area from being redlined, it may have been considered by Atlanta Life’s executives as a defense against depreciation and disinvestment. Herndon, in any case, chose to disregard the financial risks that the affordable housing project posed to his own property, located only a few blocks from Magnolia Terrace.

The Housing Act of 1961 allowed nonprofit organizations to obtain low-interest federal loans, and there followed a flurry of construction by African American churches.

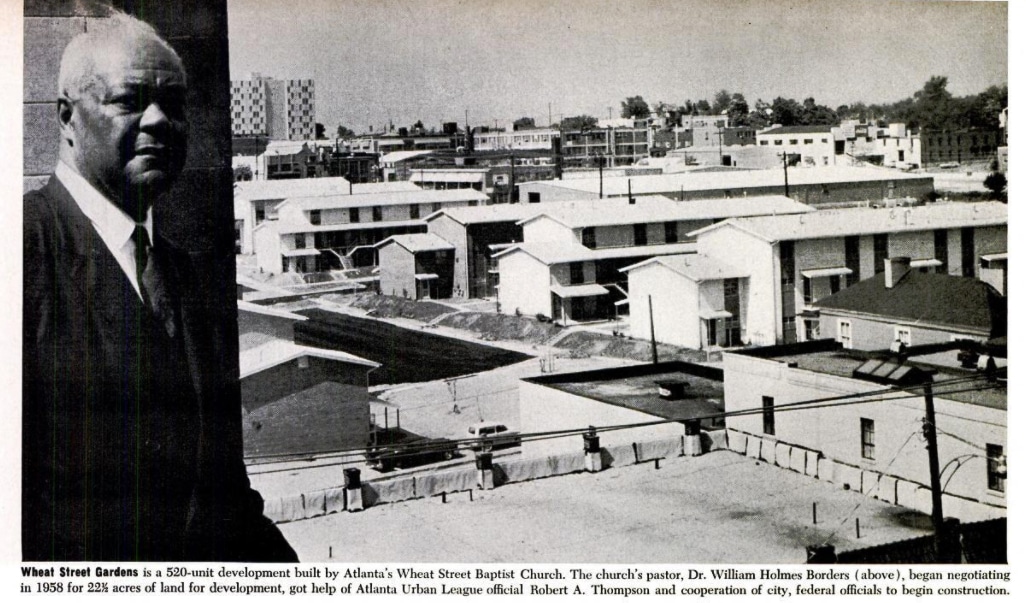

The Housing Act of 1961 allowed nonprofit organizations to obtain low-interest federal loans for new construction, and there followed over the next decade a flurry of planning and construction by African American churches and other civic institutions, who began to sponsor their own low-rise apartment complexes. 40 To take just one example, in Atlanta, the Urban League worked with civil rights activist Reverend Holmes Borders to help Wheat Street Baptist Church build a 521-unit rental development for residents displaced by slum clearance. These residents were not quite poor enough to qualify for FHA-subsidized projects, but were not wealthy enough to find decent housing elsewhere. Construction loans were backed by the FHA, while Atlanta Life loaned Wheat Street almost half a million dollars to purchase land. 41 Lending such a sum for rental housing in a poor neighborhood made little sense from an actuarial point of view. In disregarding actuarial caution, the project instigated a process I call reverse-redlining. This involved not only financing urban developments in redlined areas, but also investing in integration, existing place-based social networks, and working-class well-being. Reverse-redlined construction created affordable multi-unit housing — but not at a scale that required slum clearance, as did gigantic public housing projects sponsored by the FHA, such as Pruitt-Igoe in St. Louis and the Robert Taylor Homes in Chicago.

Reverse-redlining also involved the strategic use of corporate architectures in the struggle to expand Black neighborhoods — and, where possible, to push for integration. During the postwar boom, Golden State Mutual in Los Angeles, Universal Life in Memphis, Great Lakes Mutual in Detroit, and Dunbar Life in Cleveland all commissioned new home office buildings, while Supreme Life oversaw a major overhaul of its Chicago headquarters. NC Mutual followed with its tower. In 1980, the last major architectural commission by the Black-owned insurance industry was completed when Atlanta Life constructed a new five-story home office. While White-owned corporations were decamping for the suburbs, these companies all invested conspicuously in African American downtowns, in effect inviting other businesses, developers, and residents to follow suit.

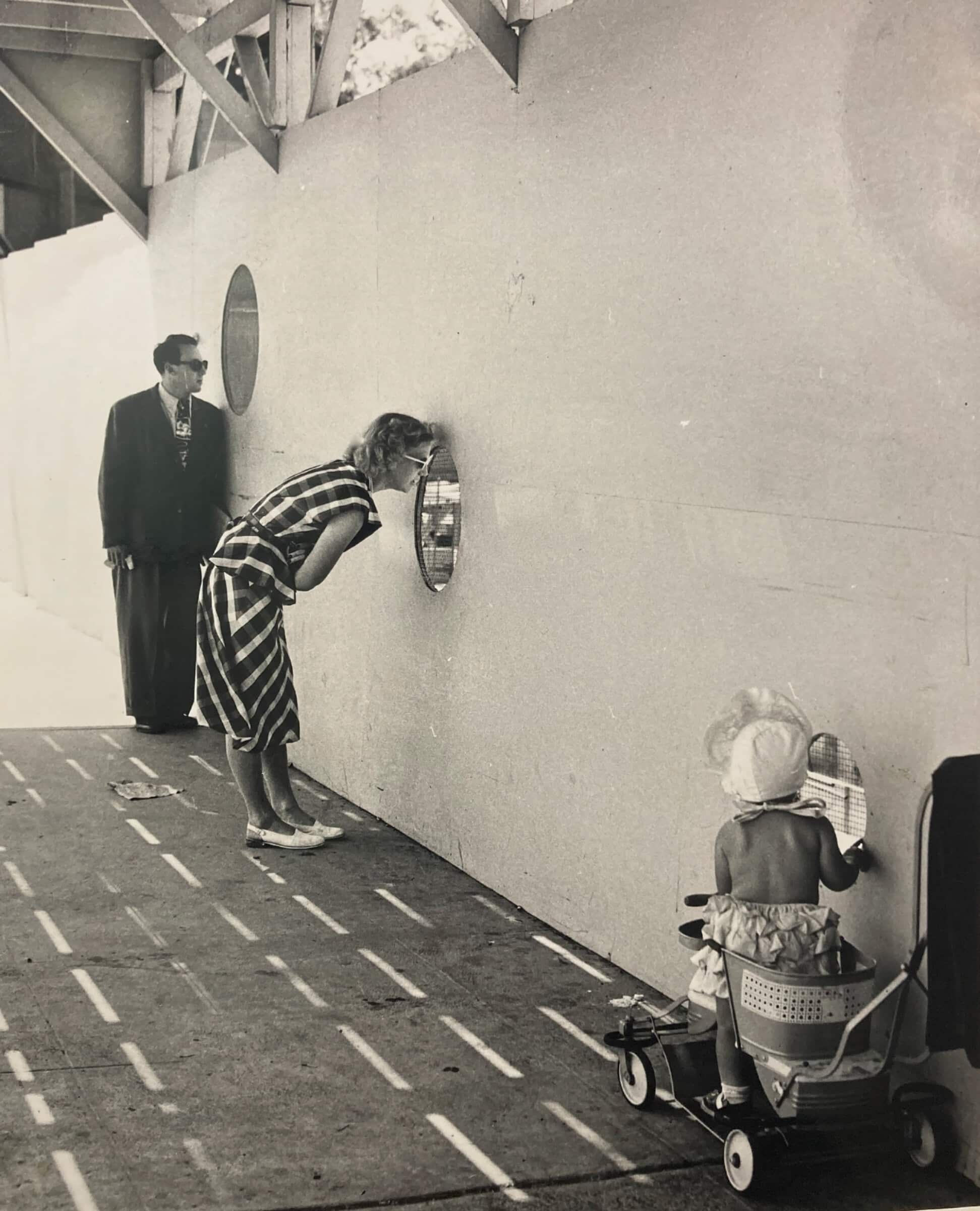

Consider a 1948 photograph taken in Los Angeles that shows a young White family peering through peepholes in a plywood fence surrounding the construction site of Golden State Mutual’s new home office. The site was two blocks south of Norman O. Houston’s Sugar Hill home. The building was designed by Paul Williams, the first African American architect to be licensed by the AIA, and the contractor was Baruch Corporation, a Jewish-owned outfit. By purchasing this building site just weeks before the 1945 court verdict that would declare Sugar Hill’s covenants unconstitutional, Golden State Mutual was erecting a kind of fortress, symbolically and materially claiming the area for African American expansion. 42

The double binds of Black capitalism were not easily escaped, however, and while the Golden State Mutual building represented racial pride in concrete form, it also attested to racialized precarity. Tour guides at the opening ceremony proclaimed:

See here the significance of the location of the building — how carefully the real estate investment was made to guarantee the safety of it .… Golden State Mutual’s home office — owned and operated by Negroes — is located at the intersection of two of the main arteries of the largest city on the West Coast. There is no shrinking here — no burying in an isolated spot in the city — but imposing, attractive placing on one of the busiest, most important corners in the city. 43

The company’s consciousness of risk extended even to their treatment of murals commissioned for the lobby, depicting African Americans’ role in colonizing and developing California. 44 Executives arranged for the artworks to be painted on canvas rather than directly onto the walls, making them portable if the company were compelled to relocate. Planning for such contingencies proved wise. The building was targeted by bomb threats in the first years of its existence; within a decade, an eight-lane interstate was plowed through Sugar Hill just a few blocks north of Golden State Mutual’s building. 45

The Black Skyscraper: Architectural Actuarialism and Black Capitalism

NC Mutual commissioned its new building in 1961, the same year that Durham’s sit-in movement began. (Asa T. Spaulding was one of two African Americans appointed by the city’s mayor, along with nine White men, to negotiate with student sit-in leaders. 46) As the tower was being planned, designed, and constructed, the March on Washington took place, Malcolm X was assassinated, and Congress passed the 1964 Civil Rights Act. The company’s five-million-dollar investment in urban real estate was thus undertaken in a period of acute uncertainty. These currents in national politics had important consequences for the African American insurance sector.

Members of the National Insurance Association knew that the anti-discrimination laws set in motion by the Act would likely impel White companies to hire Black sales staff, in order to attract a more diverse clientele — and, without the protections of a segregated market, these larger White-owned firms could bleed the African American insurance industry dry. On the other hand, by ending de jure discrimination, civil rights legislation fostered the possibility of a healthier and wealthier Black clientele, a far better actuarial prospect. Groups like the Nation of Islam were reviving the Garveyite exhortation to “buy Black,” and the Black middle class was expanding. 47 African American insurance executives had reason to hope that the challenges posed by desegregation would not spell their demise.

Civil rights legislation fostered the possibility of a healthier and wealthier Black clientele, a far better actuarial prospect.

In this moment of historical transformation, NC Mutual’s tower served to absorb the risks posed by the uncertain future. Executives chose to commission a building large enough that roughly 40 percent of its space would be leased to other tenants, allowing NC Mutual to later occupy more (or less) space, as circumstances required. As most local African American businesses were too small to rent space on the terms NC Mutual sought — just as the journalist Louis Austin had complained — both the location and the premises had to appeal to White tenants, even as the building was framed as a monument to Black achievement.

The NC Mutual Tower was thus caught between revolutionary and actuarial thinking. The building instated a form of integration in a deeply segregated city. However, to attract White tenants, the company disregarded the interests of Durham’s oldest African American neighborhood, Hayti. A planned highway would soon transect and partly demolish Hayti, severing it from the city’s Black Wall Street, which had been home to NC Mutual’s previous headquarters. Rather than lend its considerable clout to Hayti residents who were protesting the highway plan, NC Mutual chose to benefit from the slum clearance project, purchasing a site that would soon be flanked by two highway interchanges. This made the new building easily accessible from suburbs that were expanding under the impetus of the enormous new economic development project, Research Triangle Park.

When it came to hiring and wages, Spaulding and his colleagues were again cautious. Citing a lack of experience on the part of African American design firms, executives worried that hiring Black architects, contractors, or foremen would result in higher construction costs. NC Mutual wound up selecting the White-owned architectural office of Welton Becket, citing its reputation as “the hottest firm on the horizon.” 48 In deeming African American architects and contractors too risky to hire, Spaulding rehearsed the actuarial logics that reproduce structural inequalities.

A few years later, in 1963, as civil rights and labor leaders were organizing the March on Washington for Jobs and Freedom, a flood of letters arrived on Spaulding’s desk. Members of the International Hod Carriers’ Union were protesting NC Mutual’s appointment of REA as general contractor for the office tower, in light of the latter’s anti-union practices. 49 The letters pointed out that many union members were NC Mutual policyholders, leveraging the trope long vaunted by Spaulding himself: that Black firms and their policyholders constituted a community in which resources were equitably shared. Refusing to bend to the IHCU’s demands, but wishing to appease public perception, NC Mutual developed an apprenticeship program to train a small group of African Americans for work on the tower in progress.

Architect Paul R. Williams (left) with Norman O. Houston, during the construction of the Golden State Mutual, Home Office Building in Los Angeles, c. 1949. [Golden State Mutual Life Insurance Company Records. UCLA Library Special Collections, Charles E. Young Research Library, Box 61]

Golden State executives at groundbreaking ceremony for Golden State Mutual home office building in Los Angeles, 1948. From left: William Nickerson, Jr., Norman O. Houston, and George A. Beavers. [Golden State Mutual Life Insurance Company Records. UCLA Library Special Collections, Charles E. Young Research Library, Box 61, folder 13]

Construction of Golden State Mutual home office building in Los Angeles, 1948. [Golden State Mutual Life Insurance Company Records. UCLA Library Special Collections, Charles E. Young Research Library, Box 61]

Construction of Golden State Mutual home office building in Los Angeles, 1948. [Golden State Mutual Life Insurance Company Records. UCLA Library Special Collections, Charles E. Young Research Library, Box 61]

Construction of Golden State Mutual home office building, Los Angeles, c. 1948. [Golden State Mutual, Box 61, Folder 11, Golden State Mutual Life Insurance Company records (Collection 1434). UCLA Library Special Collections, Charles E. Young Research Library, University of California, Los Angeles]

Golden State Mutual Life Insurance, Los Angeles. Left: quarterly report inside GSM, 1955; right: Golden State Mutual home office building, 1949. [Left: Golden State Mutual, Box 285 Folder 3 and Box 61, Folder 11, Golden State Mutual Life Insurance Company records (Collection 1434). UCLA Library Special Collections, Charles E. Young Research Library, University of California, Los Angeles. Right: Golden State Mutual Life Insurance Company records, UCLA Library Special Collections: Box 61, Folder 1. Photographer unknown]

Golden State Mutual open house, with murals in background, 1949. [Golden State Mutual, Box 62, Folder 11, Golden State Mutual Life Insurance Company records (Collection 1434). UCLA Library Special Collections, Charles E. Young Research Library, University of California, Los Angeles]

There was urgent need to strengthen diversity in the construction industry: with the creation of Research Triangle Park, tobacco, textile, and furniture factories were closing, whereas local construction was entering a boom that would last for decades. Within a few years, North Carolina would rank second lowest in manufacturing wages nationally, and highest in its percentage of nonunion workers. 50 In offering a transitory and anti-union response to racial exclusion in the building trades, then, NC Mutual’s directors revealed the limits of their vision of Black capitalism, which offered a safety net to the working and middle classes in lieu of deeper structural correctives to inequality.

North Carolina Mutual revealed the limits of Black capitalism, which offered a safety net to the working and middle classes in lieu of deeper structural correctives to inequality.

This was distinct from the strategy adopted by Atlanta Life’s president Jesse Hill, who in the 1970s and ’80s fought to combat racism and poverty through urban development. In the mid-1970s, Atlanta Life began planning for a new office down the block from its existing home on Auburn Avenue, the central artery of Atlanta’s Black business district. Hill was, like Spaulding, a trained actuary, but his visions for urban transformation were less guided by prevailing prescriptions of risk. At a time when the U.S. was treating its older cities as collateral damage in the flight of capital to new frontiers, Hill — like Andrew F. Brimmer at the Federal Reserve Board — was a passionate supporter of what we might call Black Keynesianism (or really, desegregated Keynesianism). Advocating for public expenditure to ensure a more equitable distribution of goods and services, Hill’s approach to urban and racial politics was generally driven less by market trends and risk management practices than by a keen understanding of what these trends and policies portended for American cities if aggressive countermeasures were not taken. Hill saw clearly that 20th-century actuarial praxis was inimical to racial equality.

Hill was also an activist, serving as chairperson of the All-Citizens Registration Committee in Atlanta, trying to expand the Black vote in a city rapidly on its way to an African American majority. Hill directed the political campaign for Atlanta’s first African American mayor, Maynard Jackson, in 1974. Hill and Jackson fought to instate joint ventures between minority- and White-owned businesses, addressing obstacles to employment that civil rights legislation had failed to eliminate. And he was pivotal in the drive, in the 1970s, to establish MARTA, the city’s rapid-transit system. 51 This was symbolic as well as practical, as Atlanta’s public trollies had been targeted first by civil rights activists who fought successfully for integration, and then by Whites who boycotted and defunded the transit system. Exemplifying the quasi-statist aspects of the African American insurance industry, Atlanta Life actively intervened in the city’s economy, infrastructures, and built environment.

The Reagan Administration’s evisceration of public housing and thinly-veiled antagonism toward working-class African Americans made the decade difficult.

The company’s new building, begun in 1978, would serve as a testing ground for Hill’s vision of urban development as an instrument of integration. Hill and his colleagues selected as architectural contractors an interracial joint venture between J.W. Robinson & Associates and Thompson, Ventulett, Stainback, Inc., while the construction management contract was awarded to a partnership between Herman J. Russell — the largest African American developer in the southeast — and Batson-Cook Construction. 52 Publicity focused on these joint ventures and the project as an engine of downtown revitalization. Hill’s battles were waged, however, as Keynesian urbanism was going into a decline and neoliberal policy was taking hold, bolstered by segregationist politics. In suburban Atlanta, White segregationists refused to opt into MARTA, and its ridership and revenues were hobbled, even as the city’s highway system expanded; White-majority municipalities across the nation were similarly choosing to defund recently desegregated public services.

Atlanta Life’s new building opened its doors in 1980, the same year that President Jimmy Carter lost to Ronald Reagan. The Reagan Administration’s evisceration of public housing provisions and its thinly-veiled antagonism toward working-class African Americans and their neighborhoods made the decade difficult for the African American insurance sector. Atlanta Life and Golden State Mutual survived by dint of corporate transformation, reinsurance with larger White firms, and takeovers of other African American firms. 53 NC Mutual was especially nimble — but, nonetheless, the company sold its tower to a White developer in 2006, relinquishing the use of all but a single floor. In 2006, Golden State Mutual sold off its significant art collection and, in 2009, its home office building. In 2010, Atlanta Life sold its building to Georgia State University, an institution that Hill had fought to desegregate in 1960s. 54

Actuarial Futures and the Decline of African American Insurance

At the opening of the NC Mutual tower, Brimmer had warned of falling employment opportunities for urban African Americans. A few years later, in 1969, he coauthored with his colleague Henry Terrell an article on Black capitalism, demonstrating its vulnerability in catering primarily to the capital-poor ghetto. “The strategy,” they argued, “is appealing to white conservatives because it stresses the virtues of private enterprise capitalism as the path to economic advancement instead of reliance on public expenditures, especially for public welfare.” 55 Earl B. Dickerson, by then president of Supreme Life, voiced similar concerns to Congress in 1970, asserting that even “if all the businesses in the ghetto areas of Chicago were owned and operated by Black people, it would meet a pitifully small percentage of the employment and economic needs of our people.” 56

Major changes reshaped the insurance industry. First was the shift to group packages; next was expansion into banking services.

Brimmer attempted to avert collapse of the African American insurance industry. But he succeeded only in forestalling it, as the last remaining companies — Atlanta Life, Golden State Mutual, Chicago Metropolitan Assurance, Mammoth Life, NC Mutual, Supreme Liberty, and Universal Life — were whittled away, their buildings shuttered or purchased by other institutions. Not only had civil rights legislation inadvertently pitted Black-owned companies against larger White-owned competitors, but real wages and employment for African Americans had declined.

Two major transformations had also reshaped the U.S. insurance industry as a whole. First was the shift from a focus on individual and household policies to group packages sold to employers, a shift that favored White companies; second was companies’ expansion into more sophisticated banking services. Some Black-owned firms, like NC Mutual, experimented with financial diversification, yet few of their clients were in a position to amass substantial investment portfolios. 57 Most corporate records on foreclosures remain sealed to the public to this day. But it is safe to surmise that another reason for decline in the Black insurance sector lay in the impoverishing policies of the Reagan era, which would have led to a rash of foreclosures. 58

At the opening ceremony for the NC Mutual tower, HUD Secretary Robert C. Weaver had declared:

That building … represents the melding together of all the old components, the old materials that we have been using for a long, long time in building, but they are so brought together that we have created something new, something freer …. And, to me, that is a challenge we face in the social and political life of this country — to bring together the old elements — meld them together in new design …. Perhaps we can create… with the same materials, a society that man can be proud of and in which all can participate with freedom and dignity. 59

It comes as little surprise that companies and the individuals who ran them could not fully untangle themselves from the double bind.

Certainly, as Weaver argues, the future is built to some extent out of the past. But NC Mutual’s tower — rising, as it were, from the ashes of slum clearance in Hayti — did not suggest a radically different future. Actuarial thought, after all, does not simply build from the materials of the past. It patterns the future on the past, such that history’s violence haunts the future in the form of statistical traces and market trends. Cities across the nation bear scars of this history to this day, in sprawling expressways, industrial ruins, pollution, displacement, and disinvestment. Actuarial functions are increasingly digitized, and thereby rendered invisible. In lieu of mortality tables and redlining maps, complex algorithms now translate the past and present into a blueprint for the future while black-boxing the formulas through which this translation occurs. In this sense, the opposition between revolutionary thought and actuarial thought involves a struggle not only over the relationship between past and present but also over the processes and formulae through which people, places, and things are assigned values.

The African American insurance industry of the 20th century was caught in this struggle, vacillating between actuarial and revolutionary logics, lending its social, cultural, and economic capital to civil rights causes and reverse-redlining, but also financializing the acute biological and economic risks borne by the working classes. It comes as little surprise that companies and the individuals who ran them could not fully untangle themselves from the double bind, as the knots binding past to future — and thus linking violent histories of racial capitalism to current forms of poverty, discrimination, and violence — could not be undone through the same epistemic and economic means that had tied these things together in the first place.

{kind=link}

If you would like to comment on this article, or anything else on Places Journal, visit our Facebook page or send us a message on Twitter.